Getting your first foot on the property ladder can be tough, especially when you’re trying to save up enough money for that all-important deposit.

Thankfully, a range of high street banks offer specialised savings accounts designed to give first-time buyers a boost when saving for their deposit.

Help-to-buy ISA’s were introduced in 2015 to help first-time buyers get an easier leg-up onto the property ladder.

Through using a help-to-buy ISA, you can earn up to 2.58% interest tax-free.

Better still, the government will top-up your saving by a further 25% which could be thousands on top of what you save!

Free money AND tax-free interest sounds pretty good, right? But if you want one, you’ll have to move fast.

Help-to-Buy ISA’s are being dropped from November 30th this year in favour of a Lifetime ISA (LISA) instead.

The Money Saving Expert, Martin Lewis, is urging all first-time buyers to open an account now, even if they’re not thinking about buying a home yet.

You only need £1 to open an account with, which you can then continue to put money into when you’re ready.

The maximum you can open an account with is a £1,200 lump sum and you’re limited to putting in £200 a month.

You can be as young as 16 to open a help-to-buy ISA, whereas the new LISA will only be available to those between the ages of 18-39.

Not sure which option would be better for you?

Martin Lewis gives his opinions on help-to-buy ISA’s versus Lifetime ISA’s.

Does a help-to-buy ISA seem like the ideal option for you? Want to set up a help-to-buy ISA before the end of November? Here’s our handy guide to help-to-buy ISA’s which will take you through everything you need to know.

Simply, a help-to-buy ISA is a government scheme set up to help first-time buyers save for a mortgage deposit.

You must be classified as a first-time buyer to qualify for the scheme, which means you must not own a property anywhere in the world.

Your savings will be tax-free, as they are with any ISA product, but you’ll receive a bonus of getting Government contributions.

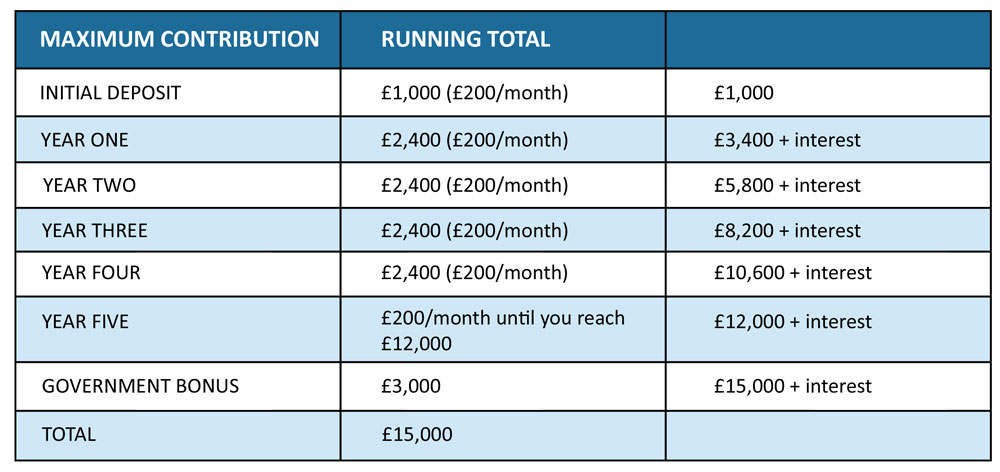

As we mentioned earlier, the government will top up any contribution you make by 25%, up to the limit of £12,000.

Although you can open a help-to-buy ISA with as little as £1, the minimum amount you need to save to qualify for the government bonus is £1,600.

If you were to save the minimum amount needed to qualify for the bonus, you’d still receive a healthy £400 on top of your savings.

You can start off your ISA with an initial deposit of up to £1,000 which also qualifies for the 25% boost from the government.

It’s also worth noting that help-to-buy ISA’s are available to each first-time buyer, not each home.

So, if you’re buying a property with your partner, for example, you’ll be able to get up to £6,000 towards your deposit.

· You need to be a first-time buyer

· You must be aged 16 or over

· You can use a help-to-buy Isa with any mortgage; you’re not restricted to a help-to-buy mortgage.

· You can use it to buy any home worth up to £250,000 (or up to £450,000 in London).

· You can’t use a help-to-buy ISA if you’re only going to rent out the property.

· You can’t use a help-to-buy ISA on an overseas property.

· You can’t have more than one help-to-buy ISA.

· You can’t open a help-to-buy ISA and a normal cash ISA in the same tax year*.

*Some providers will let you save into a cash ISA and help-to-buy ISA within the same ISA wrapper. However, the standard cash ISA and help-to-buy ISA allowance limits will still apply.

Absolutely! The government bonus will be added to your overall deposit.

You’ll need to provide evidence of the funds you have available at your initial mortgage appointment so that your advisor can calculate your overall mortgage.

This will include the amount saved into your help-to-buy ISA among other documents.

Your lender will then include the amount of your government bonus when working out your mortgage loan amount.

You can claim your government bonus once your savings have reached the minimum amount (£1,600).

If you want to achieve the maximum bonus of £3,000 it will take just over four and a half years.

It’s worth noting you need to claim your bonus through your solicitor or conveyancer before completion, but after an exchange of contracts, which might be subject to a maximum fee of £50 plus VAT.

The interest rate on your help-to-buy ISA will depend on with provider you go with.

Rates vary from each provider, so make sure you do your research before setting up your help-to-buy ISA.

You won’t earn interest on your government bonus because you don’t actually get that money until you buy your property.

When you do receive your bonus, it’s calculated using the money you’ve saved and the interest built up while your account has been open.

You can apply for a help-to-buy ISA through a bank or building society either online, by telephone or in branch.

If you’d like some friendly advice about help-to-buy ISA and where to get the best rates, get in touch with our financial services team.

Call 0161 443 4830 or click here to fill in an enquiry form.

The rules for transferring money from one help-to-buy ISA to another will be the same as a cash ISA.

You’ll be able to switch from one provider to another whenever you like. Especially as interest rates change, you’ll be able to ensure you get the best deal.

If you do decide to switch, make sure you do this carefully so you don’t accidentally withdraw money rather than transfer it.

Help-to-buy ISA’s are only available up until the 30th of November 2019.

They won’t be available to new savers after this date, however, if you already have an account set up before this date you can keeping putting money into it.

You must claim your bonus by the 1st of December 2030.

Yes. If you’ve paid into a cash ISA and want to open a help-to-buy ISA in the same tax year, you’ll need to transfer your active cash ISA to a Help-to-Buy ISA.

You can transfer up to £1,200 from your active cash ISA to your help-to-buy ISA.

The standard help-to-buy and cash ISA allowance limits still apply.

Although you could save a lot more in a Cash ISA (£20,000 in 2018/19) in comparison to a help-to-buy ISA (£2,400 plus the initial deposit) the 25% boost offered by the government is much higher than you’d earn in interest alone.

It’s also worth noting that if you’re a basic taxpayer, you’ll be able to earn tax-free interest up to £1,000 in a normal savings account (or up to £500 if you pay higher tax rate).

So, if you want to save more than £200 per month, you might want to consider saving into a top rate savings account alongside your help-to-buy ISA.

If you’d like some free, friendly advice on all things help-to-buy our highly qualified team of mortgage experts are here to help.

Call us today on 0161 0161 443 4830 or click here to fill in a contact form.

Help-to-Buy: Everything you need to know

What is Shared Ownership? Here’s everything you need to know